Understanding EPS and PF Transfer: A Comprehensive Guide

The Employee Pension Scheme (EPS) and the Provident Fund (PF) are crucial components of retirement planning in India. These two schemes, while distinct, serve the common purpose of securing the financial future of employees after their working years. EPS is designed to provide pension benefits after retirement, ensuring a steady income for retirees. In contrast, PF serves as a savings scheme, where both employees and employers contribute a portion of the salary. Navigating the intricacies of these schemes is essential, especially when transitioning from one job to another. This guide aims to elucidate the details surrounding EPS and PF, the transfer processes involved, and best practices to optimize retirement benefits.

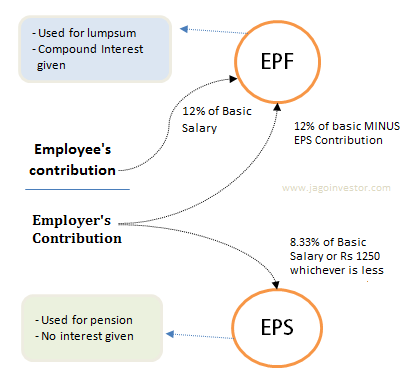

The Contribution Breakdown

Understanding the contribution structure of EPS and PF is vital for employees. The employer contributes a total of 12% of an employee’s salary to the Provident Fund. Out of this, 8.33% is diverted to the Employee Pension Scheme. This means that a significant portion of the employer’s contribution directly impacts the pension benefits an employee will receive in the future. For example, if an employee earns ₹50,000 per month, the employer’s contribution would amount to ₹6,000, of which ₹500 would go towards EPS. Employees should be aware of how these contributions accumulate over time and how they influence their retirement corpus. Moreover, it is essential to note that the contributions to EPS are capped at a salary limit of ₹15,000 per month. This implies that even if an employee earns more than this threshold, the contribution towards EPS will still be based on ₹15,000. Understanding these limits can help employees plan their finances better and set realistic expectations for retirement benefits. By analyzing the contribution breakdown, employees can make informed decisions regarding their career moves and financial planning.

Transferring PF Amounts

Changing jobs is a common occurrence in today’s dynamic work environment, and understanding how to manage PF balances during such transitions is crucial. When an employee switches jobs, they have the option to transfer their PF balance to the new employer’s EPF account. This process can be initiated online through the EPFO portal, which simplifies the transfer process. Employees need to log in with their Universal Account Number (UAN) and navigate to the ‘Transfer Request’ section. Alternatively, employees can also request the new employer to initiate the transfer. This requires filling out a form and submitting it to the HR department. Ensuring a smooth transfer of PF amounts is essential, as it allows employees to consolidate their retirement savings, avoiding the hassle of managing multiple accounts. Moreover, timely transfer prevents any delay in accessing funds during retirement, ensuring that employees can enjoy their post-retirement life without financial strain.

EPS Transfer Process

The EPS transfer process differs significantly from that of the PF. Unlike the PF amount, which can be transferred directly, the EPS amount is linked to the pensionable service from the previous employer. This means that when switching jobs, it is crucial to maintain records of the length of service with the previous employer. The pensionable service is a key factor in calculating the future pension benefits an employee will receive. To facilitate the transfer, employees must inform the new employer about their previous employment details. This information is used to link the pensionable service to the new employer’s EPS account. It is important to note that the transfer of pension credits does not happen automatically. Employees must ensure that their previous employer has updated the relevant records, which can be done through the EPFO portal. Keeping track of pensionable service is vital, as it directly impacts the amount of pension one can expect upon retirement.

Understanding Service Details

During a job change, several key service details are transferred, including the length of service and the last wages drawn. These details are crucial for calculating pension benefits under the EPS framework. Employees should make it a priority to access and verify these details to ensure accuracy in their retirement planning. To access service details, employees can log into the UAN portal, where they can view their employment history and contribution records. It is advisable to download and keep a copy of the service records, as these documents may be required for future reference. Understanding how these details affect pension calculations can empower employees to make informed decisions about their retirement. Furthermore, ensuring that all information is accurate and up-to-date can help avoid complications when claiming pension benefits.

Withdrawal and Scheme Certificates

For employees with less than 10 years of service, the option to withdraw their PF amount is available. This is particularly relevant for those who may not be able to transfer their accounts. Withdrawal benefits are typically disbursed within a few weeks of submitting the request. However, employees should be aware that withdrawing their PF amount can have long-term implications on their retirement savings. On the other hand, employees with more than 10 years of service should opt for a scheme certificate instead of withdrawing their funds. A scheme certificate allows employees to retain their pensionable service, which is crucial for calculating future pension benefits. This certificate acts as a testament to the employee’s service and can be presented to future employers when required. Understanding the differences between withdrawal benefits and scheme certificates is essential for maximizing retirement savings and ensuring a secure financial future.

Importance of Tracking EPS Status

Regularly checking EPS status is a best practice that employees should adopt. This ensures that the years of service are accurately reflected in their records, which is critical for future pension calculations. Employees can easily check their EPS status through the UAN portal, where they can monitor their contributions and service details. By maintaining oversight of their EPS status, employees can identify any discrepancies or issues early on, allowing for timely rectification. This proactive approach not only enhances the accuracy of their records but also ensures that they receive the correct pension amount upon retirement. Additionally, staying informed about contributions can help employees plan their finances more effectively, ensuring they are prepared for their post-retirement years.

Implications of Not Transferring EPS

Failing to transfer EPS service details can have serious repercussions on an employee’s future pension calculations. When employees do not complete the transfer process, they risk losing valuable pension credits that can significantly impact their retirement income. The importance of maintaining accurate records cannot be overstated, as discrepancies can lead to lower-than-expected pension benefits. Without a proper transfer, employees may face delays in receiving their pension or, in some cases, may not receive it at all. This situation can create financial strain during retirement, underscoring the necessity of completing the transfer process promptly and accurately. Employees should take the initiative to ensure that their EPS details are transferred correctly, maintaining communication with both their previous and current employers throughout the process.

Conclusion and Best Practices

In conclusion, understanding the complexities of EPS and PF transfers is vital for securing retirement benefits. Employees are encouraged to complete the necessary transfer processes diligently, maintain accurate records, and stay informed about their contributions. By doing so, they can ensure a smooth transition during job changes and safeguard their financial future. Best practices include regularly checking EPS status, familiarizing oneself with the transfer procedures, and understanding the implications of withdrawal versus scheme certificates. Taking proactive steps in managing these retirement schemes can lead to a more secure and comfortable post-retirement life. Ultimately, being informed and engaged with one’s retirement planning is the key to achieving financial stability in later years.

Your Ad Here